How to Pay Off Car Faster

We wanted to buy the best car we could afford for our family. After reviewing hundreds of vehicles, it became clear that in order to get the car we wanted, we’d need to take a loan out on it. And, if there is one thing we’re not all about, it is paying interest on depreciating “assets”.

Once we realized, we’d be paying a good chunk of change for a new car, we set out on a goal to get it paid off in a year versus five. I’m happy to share that we did it! And, I’m going to share with you exactly what we did.

A little background on us before I dive in. We are a family of four, living on one income while categorized as “middle class citizens”. While we are frugal, we are by no means extreme couponers. We simply find the best ways to stretch any and all money that comes in.

Everybody’s financial situations are different. And what worked for us and our family may not work for you.

The five things we did to pay off our car loan faster included:

- Pre-Plan the Car Purchase

- Cut Unnecessary Expenses

- Had Our Money Work for Us

- Set a Goal

- Put as much Extra Money Towards the Loan

This post may contain affiliate links. Which means that if you make a purchase through one of my links, I may receive a small commission at no additional cost to you. You can read more about this here.

1. We Pre-Planned the Car Purchase

That’s right. The first step in our process was to research as much as we could before making the purchase. We have a rule at our house that we will only carry one car payment at a time.

So, we started our search for a new car two years before paying off our other vehicle. Doing this gave us the upper hand. We (my husband) had done enough research to know when a car was overpriced, what safety precautions to look for and so much more.

He also looked up ways on how to approach salesmen and what tactics they may use. This is a very important part of the process to make sure you are not being taken advantage of.

If you already have a car loan, you might not find this step useful in your journey on paying your car loan off faster. However, for those that may not have yet made their purchase, this arguably one of the most important steps.

Because, once we knew the type of vehicle we wanted to buy, we could then work on the hard part. Saving for it. And since we would be upgrading our car to a SUV, we were going to need a sizable down payment.

We did not expect to get much from our “trade-in”. A 2005 Cobalt that my husband had been driving since high school. Therefore, the money would need to come from our personal savings account.

Initially, I had expected to be paying around $25,000 for a car, but after figuring out exactly what we wanted, we found it was going to be about $10,000 – $15,000 more.

Had we not done our research, we would’ve been shell-shocked during our car search. Which, would have led to us ending our search before being able to find the awesome deal that we eventually did find.

2. Cut Unnecessary Expenses

When we looked at expenses to cut, one of the first things to go was the TV. Given that we barely watched TV and the rise in streaming services, it just made sense. It saved us about $70 or so per month. So, not all that much, but every little bit counts, when you’re on a mission to pay something off.

Some other items that were cut back included dining out, purchasing new clothes/shoes and other miscellaneous items we didn’t really need.

Cutting these expenses really helped us save for the car in the first place. And then again, allowed us to pay off our car loan off faster – in just one year’s time.

3. Had Our Money Work for Us

I mentioned that we are on one income. The year we paid off the car, our income was NOT in the coveted “six-figures”. So, this meant that we needed to be strategic. And what we did was stretch our money and get it to work for us.

A few things we did to get the most out of the money we had was:

- Open new bank accounts to get the cash bonuses

- Utilize credit card sign on bonuses and points

- Take advantage of rebate programs, such as Rakuten

And one thing to keep in mind is that sometimes these tactics are taxable. Such as opening a bank account for the cash bonus. So, if you do decide to do this, just remember to gather those tax forms while filing the next year’s taxes.

Open New Bank Accounts to Get Cash Bonuses

This can be a hassle as many bank accounts have requirements. Things such as making monthly payroll deposits, minimum balances and such. However, sometimes the bonus is decent enough where it can make sense to take advantage of these new account bonuses.

One of the bank accounts we opened that year gave us a bonus of $400. This bonus, alone, just about paid for the interest we acquired for the year we had the car loan. So, it was as if the money was loaned to us for free. Win-win.

One thing to note is that we don’t go crazy opening bank accounts. Like I mentioned above, this money is taxable and usually categorized as “interest earned”. Not to mention, it can take quite a bit of work. Between opening the account, meeting the requirements and then remembering to close (if you choose to) the account. But, every now and then, it can give a little boost in funds.

Credit Card Sign on Bonuses and Points

When it comes to credit cards and points, I only recommend this IF you pay off your balance each month. Otherwise, all you end up doing is paying gobs of interest to the credit card companies.

We are avid credit card users and just about everything that can get charged goes on our cards. We have credit cards that give us 3-5% back of our charges each month. The cash back comes in the form of points, that we can then redeem for cash. This cash can be used for anything, including cashing in to pay off a car loan faster.

Since, we charge nearly everything to our cards we tend to gather points pretty frequently. However, I just want to stress that we do not carry over balances. Everything we charge gets paid off the following month. This is how to get the absolute most out of your credit cards.

Find yourself struggling with credit cards or scared to get one? Here’s a few tricks I did, while in college, to condition myself to use them in the best way possible. Click here to read.

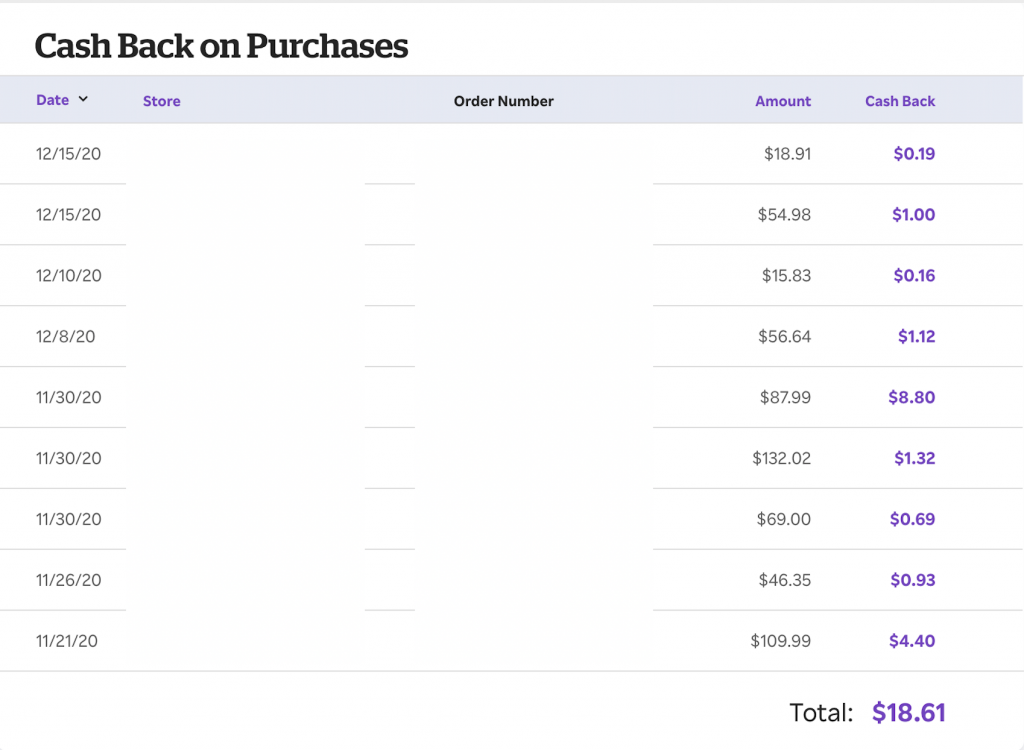

Rebate Programs, like Rakuten (formerly Ebates)

Thinking there is no way that using Rakuten is going to really help pay down a car loan faster? Theoretically, you are right. It’s not going to put a huge dent in your loan repayment. However, when you are on a mission to pay something off quickly, every dollar counts.

We use Rakuten all throughout the year, but especially during holidays, such as Christmas. As that is when huge cash back bonuses (10-20%) really come into play.

Below are screenshots of some of the cash back we have earned.

As you can see, it’s not much an astronomical amount, at all. However, it’s a totally free website to use. And when coupled in with our credit card points, really allows our money to stretch further.

If you don’t have a Rakuten account, you can sign up here.

4. Set a Goal to Pay Off Car Loan Faster

It’s easy to get so caught up just in making your monthly payments. However, when trying to pay off a car loan faster (or any loan for that matter), it’s important to not only set a goal. But to also stick to it, as much as you can.

So, what we did is we prepared a debt pay down sheet, such as the ones listed below. You’ll notice that each sheet has a “goal pay off date” and “goal payment”.

But the real benefit is in the monthly tracking. There is just something about watching a debt balance dwindle that keeps you motivated. Motivated to get it paid off as soon as possible.

If you are interested in these debt pay down and debt tracker sheets, they are both available over at my shop. The debt tracker can be found as part of 140+ page home binder. And the debt pay down is one page out of 18, from a finance planner that can be found here.

5. Put as much Extra Money Towards the Loan, as possible

The final thing we did, which is to be expected, is put as much extra money as we could towards the loan. Many months, we were able to nearly double our monthly payment. I do understand that this isn’t feasible for everyone.

However, following the theme of this post, every little bit counts.

So even if you can throw an extra $50 to the loan a month. Make one extra payment a year. Put one large payment to the loan (such as when your tax return comes or an employer bonus). It all makes a difference, in the end, and will help get the loan paid off faster.

One thing I want to note here is that you want to make sure that your extra payment is being credited to your principal amount. Our bank automatically did this, but I know from working at a bank, that all might not have this in place.

These are the five things that we did that allowed us to pay off our car loan in just a year’s time. If you have ever paid off a loan sooner than expected, let us know in the comments what you did to do so. That way we can all help each other out ?.